Interest rates look set to hold, after inflation and fuel costs fell in April. But it’s unlikely to last

Inflation actually fell in Australia last month, thanks to temporary government fuel discounts that saw fuel prices come down by 7% from their record peaks in March.

New Australian Bureau of Statistics figures show the monthly consumer price index (CPI) rose 4.2% in the 12 months to April 2026 – down from 4.6% in March and lower than market expectations.

However, the underlying picture was less reassuring.

The closely watched “trimmed mean” measure rose to 3.4%, up from 3.3% a month earlier. (The trimmed mean is the average rate of inflation after “trimming” away the items with the largest price rises or falls, leaving the weighted average of the middle 70% of items.)

Australia’s latest inflation figures will give the Reserve Bank a reason to hold interest rates steady at its June 15-16 meeting, but not a reason to relax about inflation.

With fuel prices still much higher than before the Middle East war began, the risks of further spikes in inflation and more rate rises this year have not gone away.

How fuel discounts helped cool inflation

When oil prices surged following the war in Iran, which began on February 28, the immediate effect was obvious: petrol became more expensive, soaring nearly 33% higher in March.

The new ABS data showed fuel prices actually fell 7% in April. On April 1, the federal government dropped its fuel excise by around 32 cents per litre from April 1, as well as cutting road user charges for heavy vehicles.

Both of those discounts are set to end on July 1. The government is yet to decide whether to extend them.

But central banks worry less about the initial jump in fuel prices than about how higher transport and energy costs are feeding into many other prices across the economy.

Spreading oil price shocks

According to the new data, the largest contributors to annual inflation were housing, up 6.3%, transport, up 6.6%, and food and non-alcoholic beverages, up 2.8%.

These are essential parts of household budgets, which helps explain why inflation still feels acute for many families even as the headline rate has eased.

At the same time, the rise in trimmed mean inflation to 3.4% suggests price pressures are not limited to a few volatile items in the basket of goods used to measure inflation in Australia.

Read more: What exactly is inflation, and are interest rates the only option for dealing with it?

In a speech last week, Reserve Bank Assistant Governor Sarah Hunter warned this was exactly the risk policymakers were monitoring.

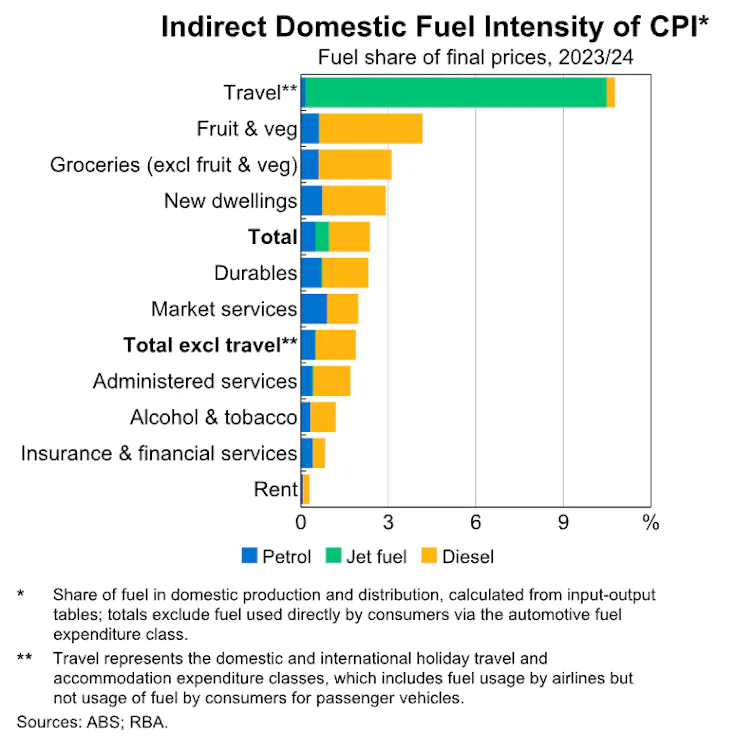

Hunter noted fuel accounts for around 2–2.5% of the cost of producing and distributing other goods and services in the CPI basket. Travel, transport and postal services, grocery items (particularly fruit and vegetables) and new home construction are all especially exposed, as Hunter highlighted with this chart.

Oil also affects inflation indirectly through global supply chains of fertilisers, plastics and other industrial inputs. So higher oil prices can eventually feed into the prices of imported goods that are not obviously energy-related.

A likely interest rate hold – for now

Last month, Reserve Bank of Australia (RBA) Governor Michele Bullock warned more interest rate hikes may be on the way to fight inflation and get it back to the bank’s target of between 2–3%.

April’s softer-than-expected headline inflation number of 4.2% will reduce the case for another immediate rate rise at the bank’s June 15-16 meeting.

However, the rise in underlying inflation to 3.4% means Bullock is unlikely to sound relaxed after that meeting. Its concerns about “second-round effects” from higher oil prices have not gone away.

The Reserve Bank now faces a difficult balancing act. Higher oil prices reduce household purchasing power and slow growth. But if businesses pass rising costs through more broadly, inflation may stay above its 2–3% target for longer. That is the classic “stagflation” dilemma central banks fear.

In its May statement on monetary policy, the Reserve Bank revised up its inflation forecasts, saying it expected headline inflation to peak at 4.8%, while underlying inflation is projected to reach 3.8%. That suggests policymakers expect the oil shock to have a more persistent effect over coming quarters.

The Reserve Bank has already increased rates three times this year, lifting the cash rate from 3.6% to 4.35%.

There are now signs the economy is softening, giving the bank’s board more reason for pause.

The latest labour force data showed the unemployment rate rose to 4.5% in April, its highest level since December 2021. This is happening as households are under pressure from high interest rates, weak real income growth and elevated living costs.

Together, these figures strengthen the case for the Reserve Bank to keep rates on hold in June. But the rise in trimmed mean inflation means the Bank is still likely to emphasise caution, rather than signal Australia’s inflation problem has passed.

Looking ahead

The next few months will be critical. If global energy markets stabilise and supply disruptions ease, some inflation pressure could fade relatively quickly. That would give the Reserve Bank more confidence that inflation is moving back towards 2–3%.

But if oil prices remain elevated, or if businesses keep passing higher transport, freight and import costs through to consumers, the inflation problem could become more persistent.

The Reserve Bank is particularly alert to the possibility that repeated global inflation shocks – first the COVID pandemic, then supply chain disruptions, and now oil prices – may gradually change how businesses and households think about inflation itself.

That is why the Reserve Bank’s focus is shifting from the direct impact of higher petrol prices to the broader behavioural response across the economy.

Today’s data was therefore reassuring, but only up to a point. The headline number was better than expected. The underlying number was not.

That’s why the Reserve Bank will be cautious about declaring victory too early.

Stella Huangfu does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.